Financial Technology, commonly known as Fintech, represents the innovative integration of technology in financial services, significantly transforming how businesses and individuals interact with money. This broad sector encompasses a wide array of products, services, and companies that aim to make financial services more accessible, efficient, and user-friendly.

What is Fintech?

Fintech refers to the use of technology to deliver financial services in novel ways, often disrupting traditional methods. This encompasses everything from mobile banking, payment processing, and online lending to more complex technologies like blockchain, cryptocurrencies, and robo-advisors. Essentially, fintech is about leveraging technological advancements to enhance the efficiency and reach of financial services.

The core objective of fintech is to simplify financial transactions, reduce costs, and broaden access to financial products and services. It has democratized finance by providing tools that allow people to manage their money, invest, borrow, and even trade in ways that were previously reserved for large financial institutions or the wealthy.

Types of Fintech Services

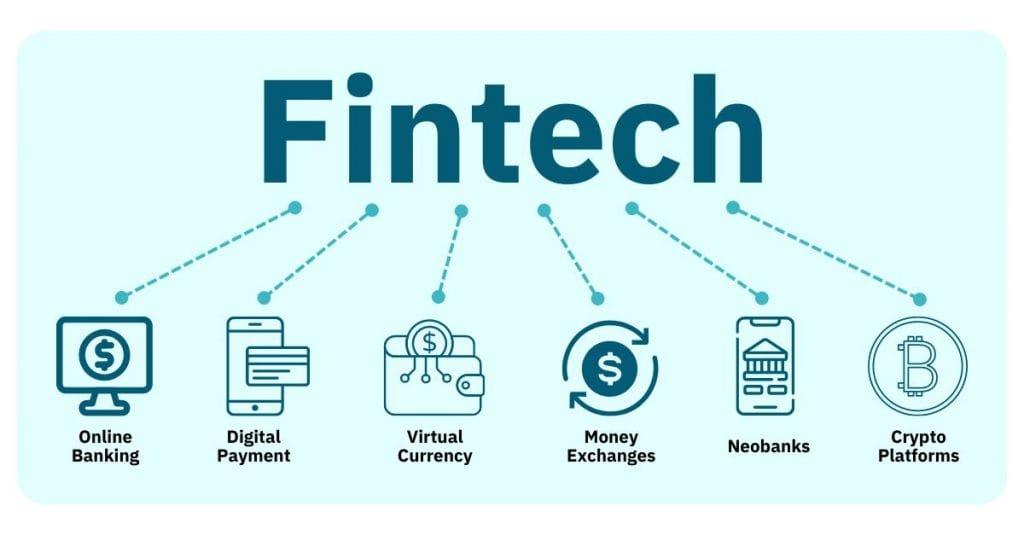

The fintech ecosystem is diverse, comprising several types of services that cater to different aspects of finance. Here are some of the most significant categories:

- Digital Payments and Transfers:

- Mobile Payments: Services like Apple Pay, Google Wallet, and PayPal have made it easier to make payments using smartphones, reducing the need for cash or cards.

- Peer-to-Peer (P2P) Transfers: Platforms like Venmo, Zelle, and Cash App allow users to transfer money directly to one another, bypassing traditional banking channels.

- Banking and Personal Finance:

- Neobanks: These are digital-only banks that operate without physical branches. Examples include Chime, N26, and Revolut, offering services like checking and savings accounts, loans, and investments, often with lower fees than traditional banks.

- Personal Finance Management: Apps like Mint and YNAB (You Need A Budget) help users track their spending, create budgets, and manage their finances.

- Lending and Credit:

- Online Lending: Platforms like LendingClub, SoFi, and Upstart provide personal and business loans directly to consumers, often with quicker approval times and better rates than traditional banks.

- Buy Now, Pay Later (BNPL): Services such as Klarna, Afterpay, and Affirm allow consumers to purchase goods and pay in installments, often without interest.

- Investment and Wealth Management:

- Robo-Advisors: Automated platforms like Betterment, Wealthfront, and Robinhood provide financial advice and investment management with minimal human intervention, typically at lower costs.

- Crowdfunding: Platforms such as Kickstarter, Indiegogo, and GoFundMe enable individuals and businesses to raise funds directly from the public.

- Cryptocurrency and Blockchain:

- Cryptocurrency Exchanges: Companies like Coinbase and Binance facilitate the buying, selling, and trading of digital currencies.

- Blockchain Solutions: Beyond cryptocurrencies, blockchain technology is used for smart contracts, supply chain management, and secure transactions across various industries.

- Insurtech:

- Insurance Platforms: Companies like Lemonade and Oscar use technology to streamline the insurance process, from underwriting to claims management, making it more accessible and user-friendly.

Participants in the Fintech Ecosystem

The fintech ecosystem is a complex network of various participants, each playing a crucial role in the development and delivery of fintech services.

- Fintech Companies:

- These are the firms that directly offer financial services through innovative technology. Companies like Square, Stripe, and Plaid have become synonymous with fintech, offering solutions that range from payment processing to financial data aggregation.

- Software Providers:

- These companies develop the technology that powers fintech applications. They offer core banking software platforms, APIs, and other tools that enable fintech companies to deliver their services. Examples include companies like Advapay and Temenos, which provide core banking system, or payment gateway providers like Adyen.

- Infrastructure Providers:

- Infrastructure providers offer the backbone on which fintech services operate. This includes cloud service providers like Amazon Web Services (AWS) and Microsoft Azure, which provide the scalable infrastructure needed to handle large volumes of transactions and data processing.

- Additionally, cybersecurity firms play a critical role in protecting the data and transactions handled by fintech companies, ensuring compliance with regulatory standards and safeguarding against fraud.

- Traditional Financial Institutions:

- Established banks and financial institutions are increasingly partnering with or acquiring fintech companies to enhance their digital offerings. They bring decades of financial expertise and customer trust to the table, which, when combined with fintech innovations, can create powerful synergies.

- Regulators and Government Bodies:

- Regulatory bodies such as the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the US, and other global entities oversee fintech operations, ensuring that they comply with laws designed to protect consumers and maintain financial stability. Regulatory bodies are responsible for issuing various types of licenses that authorize the provision of different financial services, such as MSB license, e-money or payment institution licenses, fintech licenses, and lending or crowdfunding licenses.

The Future of Fintech

The future of fintech is incredibly promising, with several trends and developments poised to further revolutionize the financial sector:

- Increased Adoption of AI and Machine Learning:

- Artificial intelligence (AI) and machine learning are expected to play a significant role in enhancing customer service through chatbots and personalized financial advice. They will also improve fraud detection, risk management, and decision-making processes within financial services.

- Expansion of Blockchain and Cryptocurrencies:

- While still a relatively new field, blockchain technology has the potential to revolutionize many aspects of finance, from transaction processing to asset management. Cryptocurrencies may become more widely accepted as stablecoins and central bank digital currencies (CBDCs) gain traction.

- Open Banking and APIs:

- Open banking, which involves sharing financial data between banks and third-party providers through APIs, will lead to more personalized and competitive financial products. This trend is likely to increase as regulatory frameworks like PSD2 in Europe continue to evolve.

- Growth in Emerging Markets:

- Fintech is likely to see significant growth in emerging markets, where traditional banking infrastructure is less developed. Mobile banking and digital payments are already making a profound impact in regions like Africa and Southeast Asia, where fintech solutions are enabling financial inclusion for millions of unbanked individuals.

- Sustainability and Ethical Fintech:

- As consumers become more environmentally conscious, fintech companies that prioritize sustainability and ethical practices will likely see increased demand. Green fintech, which focuses on financing sustainable projects and investments, is expected to grow.

- Regulatory Challenges and Innovations:

- As fintech continues to evolve, regulatory bodies will need to adapt to new challenges. Balancing innovation with consumer protection will be key, and we may see more collaborative approaches between regulators and fintech companies, fostering innovation while ensuring security and compliance.

Conclusion

Fintech is not just a buzzword; it represents a fundamental shift in how financial services are delivered and consumed. As technology continues to evolve, so too will the fintech landscape, offering new opportunities and challenges for businesses, consumers, and regulators alike. The future of fintech promises to be dynamic, inclusive, and integral to the global economy, as it continues to break down barriers and create more efficient, accessible, and innovative financial systems.