Should you put your money into savings or investments? Is it better to invest or save your money? When figuring out the most excellent approach to build your money, it’s easy to wander in circles.

Because selecting which is the best method for increasing your money might be difficult, we’ve put up a guide to help you make an informed decision. Take a step back and consider what you want to get out of your money. Whether to save or invest should become more apparent in a matter of minutes.

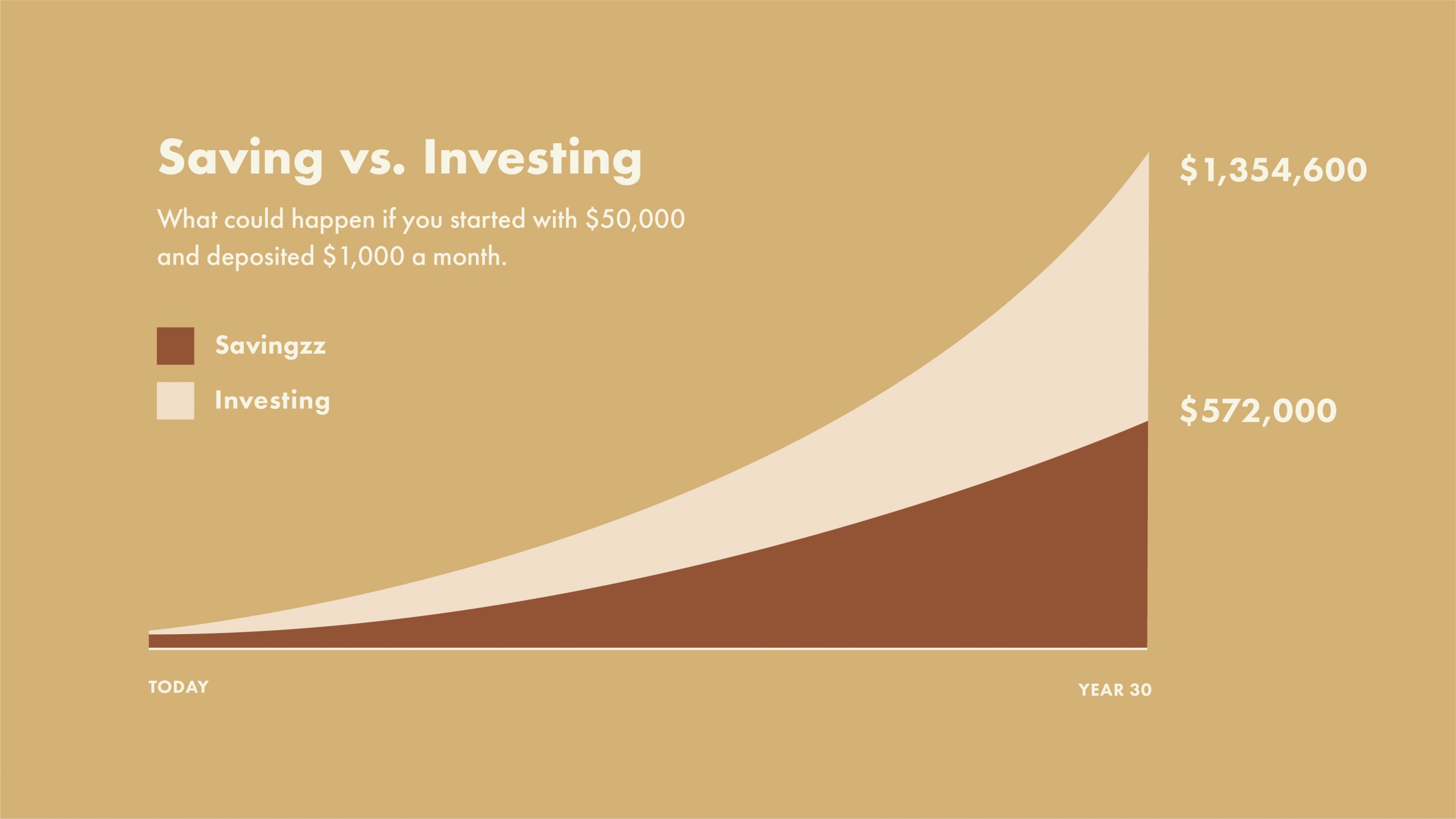

What exactly is saving?

Putting money aside for the future is referred to as saving. You can contribute to your savings account once or on a regular basis. And, if you use an easy-access account, you can get your money back – plus any interest – anytime you want it.

Is it risk-free? No, not at all. Because interest rates have been low for a long time, the return on your money will be pretty low. Inflation will not outperform inflation. While your savings account isn’t going anywhere, its purchasing power erodes over time.

What exactly is investing?

Investing, like saving, is putting money away for the future. There are several methods to invest, which entail some form of fee or tax. Shares – where you buy a little piece of a firm – and funds – already made investments that are managed by professionals – are two of the most well-known.

Investing is placing money into something that you feel will appreciate over time. You’re exposed to a different form of risk here: market exposure, which means the value of your investment can and will fluctuate, and you may receive less than you put in. Expected returns are likewise subject to change and cannot be guaranteed.

A longer time frame gives your investment more chances to recover if it loses value. And taking a calibrated level of risk allows you to generate more money than you could in a savings account.

Which one is the best fit for you?

It’s just a matter of deciding whatever combination is best for you. Of course, life is full of a variety of wants and desires. As a consequence, there’s a good possibility you’ve got a lot of financial goals in mind.

Working out how much you can afford to save each month is an excellent place to start. When you have a figure in mind, you may consider dividing it up so that you have enough money for various stages of your life. How you do so will be determined by your age and priorities.

It’s a good idea to divide your money into several pots:

Unexpected events may occur at any time.

Before you save for anything else, you should start by putting money aside for an emergency fund that you may use if something goes wrong. This should be saved in a convenient-to-access savings account with no money transfers.

What do you want to accomplish in the next five years?

Saving makes sense for the money you’ll need in the short future, such as a deposit on a house, but if you invest for less than five years, your investment may not have enough time to recover any losses in value. People tend to save money in stocks, cryptocurrency, real state etc depending upon their needs.

Things you want to do in the next 5 to 10 years.

Savings may make sense for medium-term money, such as for a child’s wedding, but investing might yield a higher return on your money if you’re willing to take a chance.

Things you’d want to undertake in the next ten years

Taking a degree of investment risk for the money you won’t need for years, such as a place to retire to, might offer you a higher return – because the value of your money will be destroyed over time by inflation if you save.