In today’s fast-paced world, managing personal finances effectively is crucial for staying on top of your financial goals. With more options available to consumers than ever before, deciding between Buy Now, Pay Later (BNPL) services and traditional lending methods can be challenging. Whether you’re purchasing essential goods, making a big-ticket buy, or simply managing monthly cash flow, understanding the differences between these two options can save you time, money, and stress.

Here are some key insights, along with practical tips and tricks, to help you make informed financial decisions.

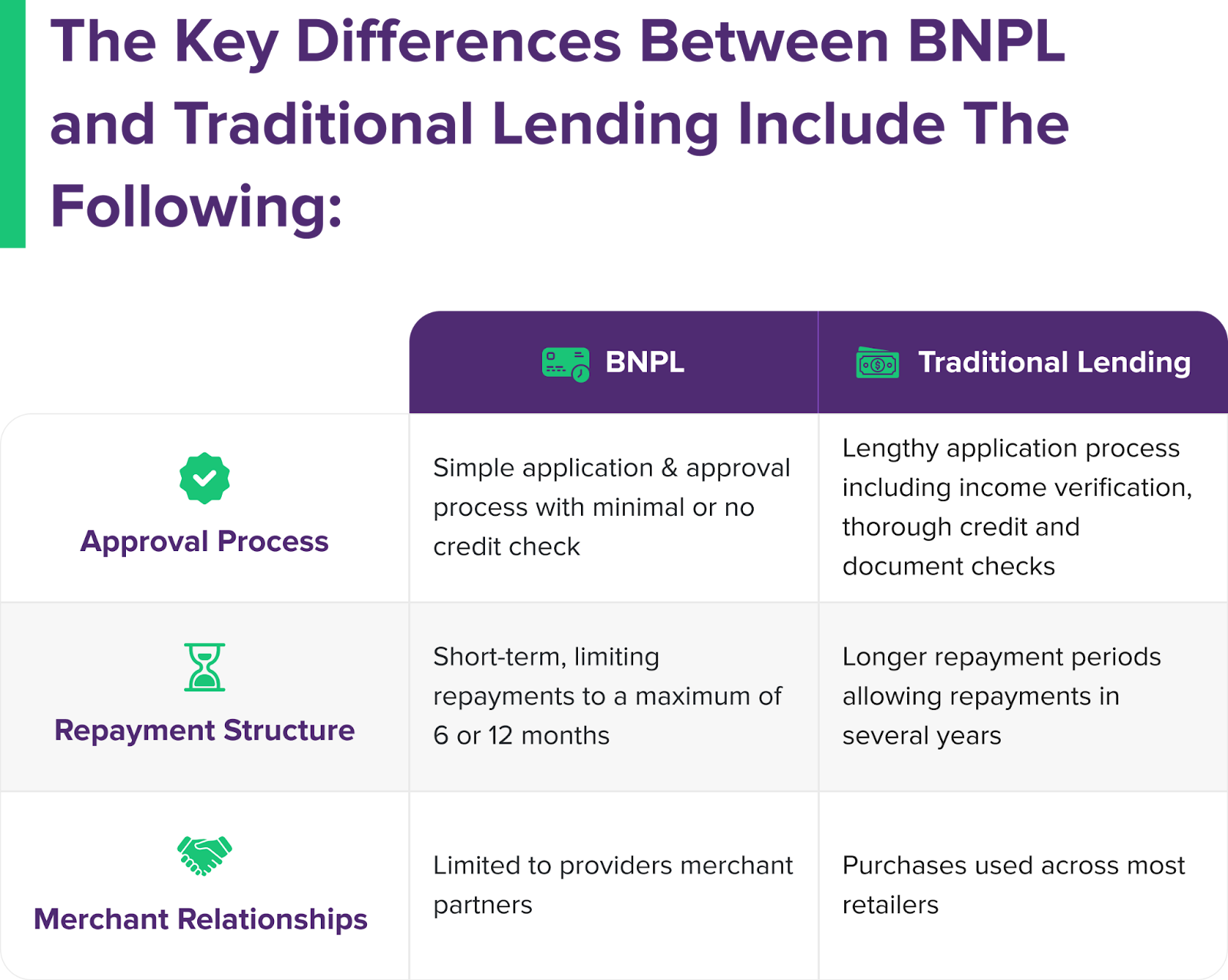

1. Approval Process: Convenience vs. Scrutiny

- BNPL: Offers a simple application and approval process with minimal or no credit check. This means you can get approved almost instantly with just your phone number or email.

- Traditional Lending: Requires a lengthy approval process, including income verification, thorough credit checks, and more detailed documentation.

Tip:

If you need to make a quick purchase but don’t have time for a long application process, BNPL is the way to go. However, always be cautious about taking on multiple BNPL accounts, as it can become difficult to track payments. For larger, long-term purchases, traditional lending offers more security and accountability through thorough checks and larger borrowing limits.

2. Repayment Structure: Short-Term vs. Long-Term Commitment

- BNPL: Repayment is typically short-term, limiting repayments to a maximum of 6 or 12 months. You’ll often find that you can spread payments over a few installments, making it easy to manage smaller purchases.

- Traditional Lending: Repayment structures with credit cards or loans allow for much longer periods—years in many cases—which can be useful for large, long-term purchases like home renovations or vehicle financing.

Tip:

Use BNPL for smaller, more manageable purchases that can be paid off quickly. For bigger expenses, it’s better to go with traditional lending options that offer more time to repay. Additionally, always choose a repayment plan that you’re confident you can handle to avoid late fees or negative impacts on your credit score.

3. Interest Rates and Fees: A Battle Between Low Cost and High Interest

- BNPL: Many BNPL services offer interest-free installment plans, provided you meet the payment schedule on time. However, missing payments can lead to late fees that add up quickly.

- Traditional Lending: Credit cards and loans typically come with higher interest rates, but you get more flexibility on when and how much you pay monthly. However, be aware of the compounding interest if you carry a balance for too long.

Tip:

If you can commit to paying off your BNPL installments on time, this can be a great interest-free option. If you know you might need longer to pay off a balance or anticipate carrying debt over several months, traditional lending with flexible payments could prevent costly late fees.

4. Merchant Relationships: Limited vs. Wide Acceptance

- BNPL: Most BNPL services are limited to specific merchants that have partnered with the provider. If you’re using BNPL, you need to make sure the store or service you’re purchasing from supports it.

- Traditional Lending: Credit cards and loans are widely accepted at nearly all merchants, offering much more flexibility when it comes to where and how you spend.

Tip:

If you’re purchasing from a retailer that accepts BNPL, take advantage of the flexibility. However, if you’re making purchases at multiple stores or are unsure about BNPL acceptance, your credit card might offer better flexibility and wider acceptance.

5. Credit Building: BNPL’s Advantage Over Traditional Lending

- BNPL: Unlike credit cards, most BNPL services don’t report payment activity to credit bureaus, meaning it won’t help (or hurt) your credit score.

- Traditional Lending: Timely payments on traditional credit cards and loans are reported to credit bureaus, which can help build your credit score over time if managed properly.

Tip:

If you’re looking to improve or build your credit score, traditional lending options are more beneficial. For those who already have a stable credit score and want to avoid accumulating too much debt, BNPL can be a more convenient option for short-term, interest-free purchases.

Conclusion: Which Option Is Best for You?

When it comes to choosing between BNPL and traditional lending, the best option depends on your specific financial needs and goals. BNPL is a great tool for those looking to make smaller, quick purchases with little hassle and no interest—just make sure to stay on top of your payments to avoid late fees. For larger, long-term purchases, or for building credit over time, traditional lending offers more structured repayment options and flexibility.

Use these tips to weigh your options carefully, and always make sure you fully understand the repayment terms before making any financial commitments.

This comparison between Buy Now, Pay Later services and traditional lending methods was originally published by ROSHI, a leading fintech company in Southeast Asia. Focused on digital financial solutions, ROSHI has become a preferred platform for Singaporeans seeking consumer lending services. Their product range extends from comparing home loan rates to urgent cash loans today, reflecting ROSHI’s commitment to meeting the diverse financial needs of consumers in Singapore.